The Missing Middle of Industrialization: Everything is Chemicals

It is March 1st, 2026, and the United States is in the middle of an industrialization movement unlike anything since the 1940s.

This movement has many names.

Reindustrialization.

American Dynamism.

Atoms, not bits.

If you are on X, you likely have seen these phrases in heavy rotation, especially over the past few weeks. Venture capital is waking up t the world of matter. You have possibly seen me talk about American Creatine, and the criticality of the supply chain.

Especially with the breakthroughs being achieved weekly by LLMs, and the reality of software becoming abundant and cheap, this has produced a growing realization that the frontier of power is shifting back to the physical world.

AI makes code cheap. It does not make chemicals, metals, or materials.

And AI has immense material needs of its own. Data centers are enormous physical undertakings, requiring space, power, cooling, construction, and the chips that every nation on Earth is competing for. They are a perfect example that the constraints on the future of abundance have become physical.

What does it take to make things?

That question is the heart of industrialization. We need clarity around the answers.

My deep dive into this problem led to a simple realization.

America does not have an innovation problem. What we have is a production problem. An enormous one.

But not unsolvable.

The United States leads the world in R&D spending, accounting for roughly 30% of global investment, but we have lost the production of the very technologies we once invented, and continue to invent.

This gap is what I deemed the Missing Middle. It is the space between raw materials and precursors, and finished products and production. It spans capital, the workforce, and technology adoption.

Rebuilding in this space is the precondition for everything else the industrialization movement is trying to achieve.

Closing it will become the defining industrial challenge of our era.

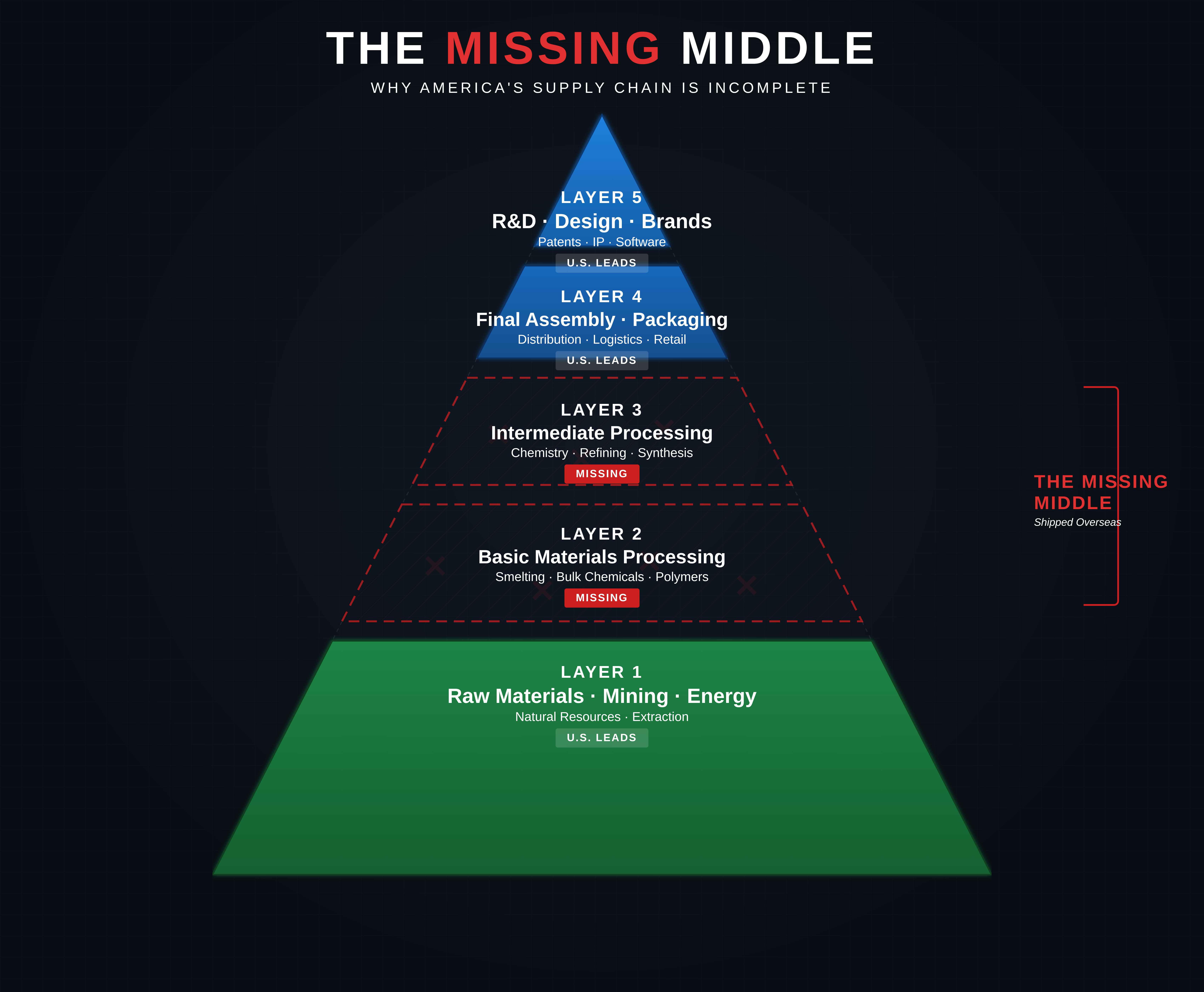

Defining the Missing Middle

Every manufactured product sits atop a pyramid of value creation. Five layers, each one depending on the layer below it.

Layer 5 R&D, Design, and Brands. The apex. This is where ideas become intellectual property; patents, product designs, brand identities, software architectures. America dominates here. The best universities, the deepest venture capital pools, the strongest patent portfolios on the planet. Pfizer, Apple, Google, Dow’s research labs. This is the layer that gets celebrated.

Layer 4 Final Assembly, Packaging, and Distribution. The layer where finished products come together and reach consumers. America is strong here too; Amazon’s logistics network, UPS, FedEx, the largest consumer market on Earth. Factories that bolt together components, fill bottles, shrink-wrap pallets, and ship.

Layer 3 Intermediate Processing and Fabrication. This is where basic materials become specialized. Refining. Synthesis. Precision chemistry. The steps that turn bulk alloys into aerospace-grade titanium specifications, commodity chemicals into active pharmaceutical ingredients, base polymers into semiconductor-grade photoresists, precursor compounds into the intermediates that feed circuit boards, propellants, and battery cells. This is also where the production ecosystem compounds; the more volume you run, the more integrated processes become, the faster you iterate, and the faster costs fall. Economies of scale in intermediate processing are not theoretical. They are the reason China dominates: decades of throughput created cost advantages that no startup can match on day one. You have to build them.

Layer 2 Basic Materials and Commodity Processing. Bulk chemical production. Primary metal smelting. Rare earth separation and refining. Basic polymer manufacturing. The large-scale conversion of raw inputs into standard industrial materials; ammonia, ethylene, pig iron, caustic soda, rare earth oxides, battery-grade lithium carbonate. This is the world of chemical and metallurgical engineering at volume: massive reactors, solvent extraction circuits, continuous processes, tight energy margins. Rare earth processing sits squarely here—the U.S. can mines rare earth minerals and ore, but they get shipped to China for separation because we have lack domestic capacity to perform the hydrometallurgical steps that turn raw concentrate into individual oxide products. The output at Layer 2 is not specialized, but everything specialized depends on it.

Layer 1 Raw Materials, Mining, and Energy. The base. Natural resources, mineral extraction, oil and gas, agricultural feedstocks. America has enormous endowments here; Permian Basin hydrocarbons, Appalachian minerals, Nevada lithium, Montana antimony, some of the richest natural resource deposits on Earth.

America is strong at the top of the pyramid. It is strong at the base.

But it is Layers 2 and 3 where the gaps become obvious. The US is structurally absent across dozens of critical categories.

You dont get Layer 3 without Layer 2

The Missing Middle is invisible because intermediates have no recognizable brand, no consumer constituency, and no political champion. You take creatine, you do not think about the sarcosine and cyanamide that were reacted to produce it. You take a prescription drug, you do not think about the API synthesized in Zhejiang Province. You use a smartphone, you do not think about the DCD-cured PCB laminates sourced from Ningxia.

This invisibility creates a dangerous assumption: that the supply chain works because it has always worked.

Andreessen Horowitz recently published an analysis they call "Everything is Computer"

Their thesis is for building the "modular middle" of the electro-industrial supply chain, the integration layer where commodity components become functional subsystems like battery packs, motor assemblies, and PCB boards.

This is the layer that determines technological and geopolitical dominance.

China mastered this layer while America abandoned it.

They are right on both points.

But their analysis contains a critical blind spot: it treats the inputs to the modular middle as a solved problem.

"The upstream materials and device primitives we need are, for the most part, increasingly available,"

This is a load-bearing assumption of their entire thesis, and its not correct.

If we trace their own examples one layer down

—>The battery packs they want assembled in America require battery-grade graphite, refined lithium, and manganese sulfate.

-Battery-grade graphite processing had zero U.S. capacity until Syrah Resources opened a single facility in Louisiana in 2024, the first outside China.

-Refined lithium production is limited, Albemarle operates Silver Peak in Nevada, Arcadium Lithium runs a facility in North Carolina, and Tesla’s lithium refinery in Corpus Christi just became operational in January 2026 as the first spodumene-to-lithium-hydroxide plant in North America.

But total U.S. refined lithium output remains a fraction of global demand, and these expansions have only emerged in the last three years.

-Battery-grade manganese sulfate: zero U.S. production currently.

China controls 97% globally. Facilities are in development but none are operational.

—>The drone and EV motors require NdFeB permanent magnets.

-China manufactures roughly 90% of the global supply.

MP Materials opened the first U.S. NdFeB magnet facility in Fort Worth in early 2025, producing approximately 1,000 tons per year against China’s 100,000-plus.

-The PCB substrates require dicyandiamide as the epoxy hardener in the laminate.

AlzChem in Germany operates the only DCD plant outside of China. There is Zero U.S. production.

-The semiconductor chips require guanidinate precursors for thin-film deposition and fluorinated gases for etching, both concentrated in Asia-Pacific production.

The Modular requires the chemical.

The chemical industry is not just another manufacturing sector. It is the upstream layer 2 platform every other sector depends on.

The American Chemistry Council reports that while chemistry directly accounts for just over 1% of GDP, it supports roughly 25% of total U.S. GDP when you include the downstream industries that depend on chemical inputs, automotive, electronics, construction, agriculture, pharmaceuticals, consumer goods.

More than 4 million American jobs depend on the chemical supply chain. Every dollar of chemical production generates an additional $4.20 in GDP elsewhere in the economy — a total multiplier of 5.2x, the highest of any manufacturing sector.

Every one person directly employed in chemical manufacturing supports more than six additional jobs.

When you lose the chemical middle, you do not just lose chemical factories. You lose the multiplier. You lose the jobs that the jobs create. You lose the option to manufacture domestically in every sector that depends on chemistry—which is nearly all of them.

What Chemicals are we talking about here?

This is by no means an exhaustive list or complete picture of the entirety of American Industry. But it will give you the scope and scale of what we need to tackle head on. Feel free to skip this section as well, it is lengthy.

Intermediate Nitrogen Chemistry

The gap I know best, because it is the one I am building a company to fill (Athanor Inc). The United States has zero domestic production of every node in the cyanamide value chain.

Calcium cyanamide : the foundational precursor. China controls 55–75% of global capacity by most estimates, with some analyses placing it as high as 90%, it is concentrated in Ningxia province. The rest is made in Germany. Zero U.S. production.

From cyanamide, the tree branches into…

Dicyandiamide (DCD): the epoxy hardener in virtually every FR-4 PCB laminate on Earth, and the precursor to metformin, the most prescribed diabetes drug globally. 100% import dependent. Alzchem is the only western company that makes it. Zero U.S. production.

Guanidine nitrates: used in airbag gas generators, seat belt tensioners, and as the direct precursor to nitroguanidine. Zero U.S. production.

Nitroguanidine: the energetic backbone of triple-base gun propellants for 155mm artillery and insensitive munitions like IMX-101. The DoD has committed $150 million to potentially build an AlzChem-operated facility in the U.S. by 2029. 100% import dependent. Zero U.S. production.

Sarcosine: A creatine precursor, but also a surfactant feedstock and semiconductor CMP slurry ingredient. Zero U.S. production.

Creatine monohydrate: a $3+ billion global market where roughly 90% of production is Chinese. Zero U.S. production.

Policy response: Cyanamide is currently on the list of Essential Chemicals. The cyanamide gap however is invisible to Washington because the critical applications are several synthesis steps removed from the end products policymakers recognize.

Energetics and Munitions Precursors

The ammunition supply chain has the most urgent gaps and the most recent policy attention, but remains far from solved.

Nitrocellulose: the base material for gunpowder, is produced domestically but falls short of demand. China is the world’s largest producer. Russia purchased over 1,300 tonnes from China in 2023 alone.

TNT: the United States has not produced its own TNT for decades. A new facility is planned in Kentucky. Current supply depends on global sourcing with China excluded by policy. Prices have quadrupled in four years.

Antimony: a critical alloying and flame retardant element. The U.S. was 80%+ import reliant. Then in September 2024, China cut exports by 97%. Prices surged above $40,000 per ton. The Pentagon deployed approximately $1 billion in October 2025 to secure stockpiles. Domestic production is expanding in Montana but independence is not expected before 2027.

Active Pharmaceutical Ingredients

The pharmaceutical gap is the broadest in scope and the most dangerous for civilian populations.

More than 80% of APIs for essential medicines have no U.S. manufacturing source.

Less than 5% of large-scale global API production sites are located in the United States.

72% of API facilities supplying the American market are overseas.

The specific drug dependencies are extensive.

Ibuprofen: 95% import dependent

Hydrocortisone: 91%.

Antibiotics: 80%.

Acetaminophen: 70%.

Heparin crude: 80%.

The United States has zero domestic fermentation manufacturing capability for antibiotic APIs. The last American penicillin production ceased in 2004.

Metformin: the most prescribed drug in the world for type 2 diabetes, traces its precursor chain through DCD, which traces through cyanamide, which traces through Ningxia. The same chokepoint.

Policy response: Fragmented. The BIOSECURE Act passed the House but stalled in the Senate. A Strategic API Reserve executive order exists. Section 232 tariffs on drug imports are under discussion. But no comprehensive reshoring program exists for upstream chemical synthesis.

Rare Earth Processing

China is in control here

85% of global rare earth refining

91% of magnet rare earth processing

90% of NdFeB permanent magnet manufacturing.

The U.S. gap spans the entire midstream-to-downstream chain.

Heavy rare earths like dysprosium and terbium have near-zero American production. A handful of facilities are under development, REalloys in Ohio, USA Rare Earth in Oklahoma, but China produced over 320,000 tonnes of rare earth oxides last year versus roughly 67,000 in the United States.

Policy response: The $12 billion Project Vault critical minerals stockpile launched in February 2026. But refining is what is needed over all else

Battery Materials

Battery-grade graphite: China controls 75–95% of global processing.

Battery-grade manganese sulfate: Zero U.S. production. China controls 97% globally. The U.S. has not produced primary manganese ore since the 1970s.

Primary nickel refining: Zero U.S. production.

Cobalt refining: minimal.

Lithium refining to battery grade: less than 2% of global supply. Only 3 of 66 proposed U.S. lithium extraction projects are under construction.

Policy Response: $6 Billion in BIL grants + 45X production tax credits + escalating FEOC content requirements. Ironically the The FEOC requirements are actually creating a crisis because they mandate domestic or allied sourcing on a timeline that the upstream processing capacity cannot meet.

Semiconductor Upstream Chemicals

DCD: the epoxy hardener from the cyanamide tree — cures the laminates in every PCB substrate globally. 100% import dependent. Sourced from China or AlzChem.

Guanidinate ligands for ALD/CVD thin-film deposition — used to deposit critical materials at sub-7nm nodes — derive from the cyanamide tree. Electronic-grade cyanamide solutions are marketed by Ningxia producers specifically for semiconductor applications.

Fluorinated gases: essential for etching and chamber cleaning are concentrated in Asia-Pacific production. PFAS and fluoropolymers, which the DoD confirms are irreplaceable for semiconductor fabrication (replacing them “could be a 25-year effort and may not succeed in all respects”), are seeing domestic manufacturers exit the market due to regulatory pressure, potentially forcing reliance on Chinese sources.

Policy response: The CHIPS Act committed $52 billion to fab construction and workforce development. It allocated nothing to domestic production of the upstream chemicals — laminates, deposition precursors, etch gases, electronic-grade solvents — that those fabs require to operate.

Critical Minerals with Zero Domestic Production

Gallium: 100% import reliant. China controls roughly 98% of global production. Used in GaAs/GaN chips, 5G infrastructure, radar, and LEDs.

Indium: 100% import reliant. China controls roughly 70%. Used in touchscreens, infrared and night vision systems, and missile guidance.

Natural graphite: 100% import reliant. China controls roughly 70% of mining and 95% of processing.

Manganese: 100% import reliant.

Fluorspar: 100% import reliant.

Germanium: more than 50% import reliant, with China controlling roughly 60% globally.

Policy response: Executive Orders in 2025 fast-tracked permitting and opened federal lands for critical mineral mining and processing, and the DOE announced $6 million for gallium recovery R&D. China's suspension of its export bans on gallium, germanium, and antimony, paused only until November 2026 as a trade negotiation concession, is currently the primary reason these materials are still flowing to the United States at all.

Strategic Metals and Nuclear Fuel

Aerospace-grade titanium sponge: The last U.S. production facility closed in 2020. America is now 100% import reliant for the feedstock of every military jet engine, every submarine hull, and every spacecraft structure it builds.

China’s share of global titanium metals jumped from 40% in 2019 to over 75% in 2025.

Enriched uranium: Russia supplies approximately 25% of U.S. reactor fuel. A ban phases in by 2028, but domestic enrichment covers only 30–35% of requirements. The gap cannot be closed by 2030 even under optimistic scenarios.

Agricultural Chemical Inputs

Elemental phosphorus: single domestic producer, insufficient for national needs. The Defense Production Act was invoked in February 2026.

Glyphosate: single domestic producer (Bayer). Large generic volumes imported from China. DPA invoked alongside phosphorus.

Potash: the U.S. produces roughly 5% of its needs. Import reliance at approximately 94%.

Hydrogen cyanamide: the dormancy agent used on grapes, kiwifruit, and blueberries, derives from the cyanamide tree. Zero U.S. production.

How and Where to Prioritize: A Framework for Action

Ive talked about the scale of the problem, and shown dozens examples across the entire industrial economy. We cannot rebuild all of it at once. The question, the question that matters for anyone allocating capital, policy attention, or workforce investment is straightforward:

where do you start?

This took some time for me to define. After pouring over many many papers on manufacturing, chemicals, and trade policy, I realized a scoring system could be developed. Feed this into an LLM, let it run analysis, double check it works, and now you have structured data and can begin making sense of a previously opaque landscape.

While this may not be in the spirit of adventurous capitalism, it provides objectivity to both government, investors, and founders.

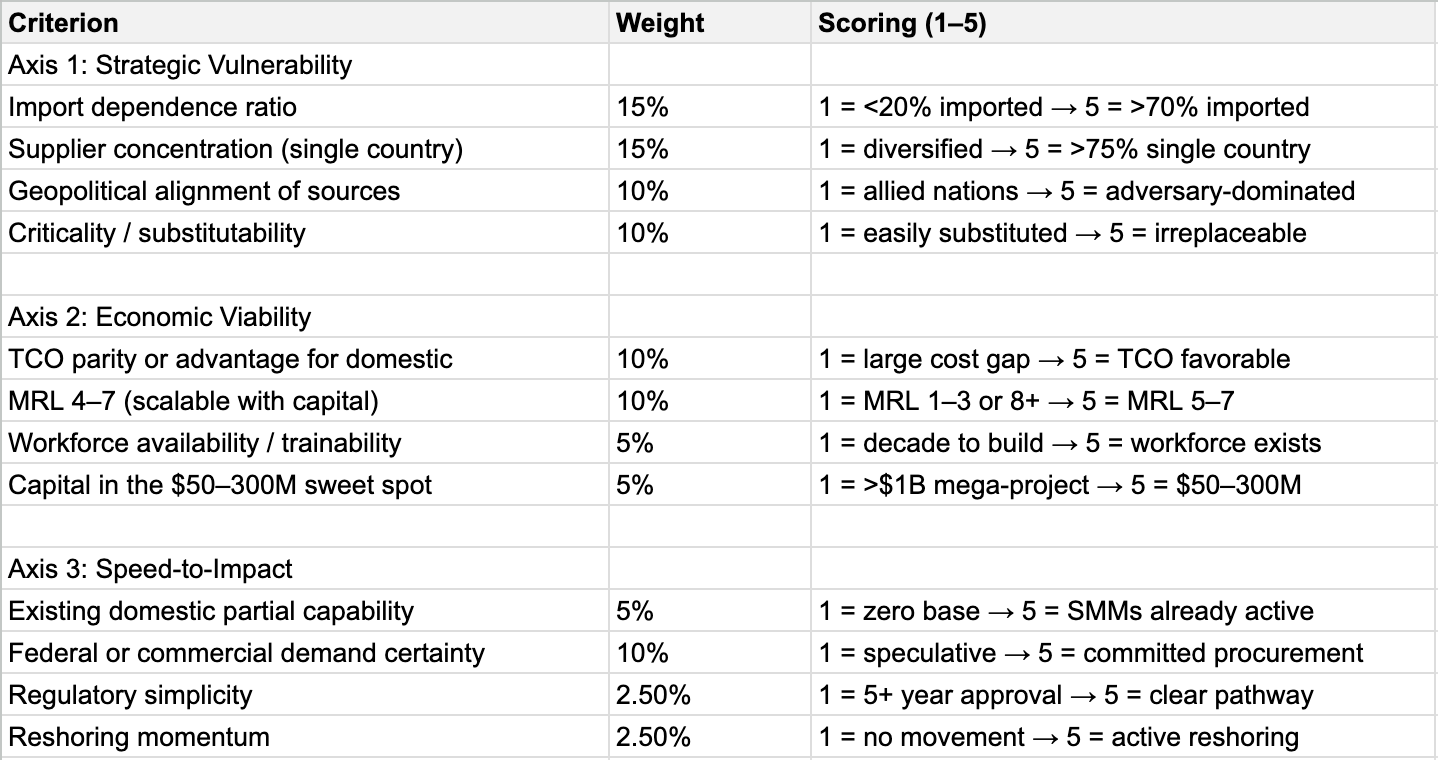

This assessment system is built on 3 Axis.

Axis 1: Strategic Vulnerability (How badly do we need this?)

This axis measures the national consequence of continued dependence.

Key Inputs:

Import dependence ratio—The share of a product’s inputs sourced from abroad. Pharmaceuticals source over 50% from foreign suppliers; motor vehicles vary by component. The U.S. is 100% import-reliant for 15 critical minerals and over 50% reliant for 46.

Supplier concentration—Measured via Herfindahl-Hirschman Index. A product sourced 75%+ from a single country (e.g., cyanamide from China, rare earth processing from China) scores maximum risk.

Geopolitical alignment—Inputs sourced from China and rest of Asia/Pacific score highest risk; allied nations (Canada, Mexico, Europe, Japan) score lowest.

Criticality / substitutability—The Fed’s key insight: semiconductors are only 5% of automobile input costs, yet their shortage shut down the entire industry. Inputs that are low-cost but irreplaceable score disproportionately high.

Defense industrial base dependency—Does DoD require this product? The consolidation from 51 defense primes to 5 means mid-tier suppliers are the actual bottleneck.

Axis 2: Economic Viability (Can this actually be done here?)

Key Inputs:

This axis prevents the mistake of trying to reshore everything at once, which is neither possible nor desirable.

Total Cost of Ownership (TCO) gap—The Reshoring Initiative’s TCO Estimator accounts for 30+ cost factors beyond FOB price, including freight, inventory carrying costs, quality risk, IP risk, and travel. Most companies miscalculate offshoring costs by 20–30% when using price alone. Products where TCO analysis shows rough parity or advantage for domestic production are the best candidates.

Manufacturing Readiness Level (MRL)—DoD’s 10-level scale from concept to full-rate production. The biggest gap is MRL 4–7: the transition from lab-validated technology to pilot-line capability. Products sitting in this range are exactly the “missing middle” — proven enough to de-risk, but not yet funded to scale.

Workforce feasibility—Does the region have (or can it develop within 2–3 years) the skilled labor? Community college manufacturing academies are already scaling in states like Illinois. Products that can leverage existing workforce ecosystems score higher.

Capital intensity vs. leverage—The OSC loan program showed 9:1 oversubscription at $10–150M loan sizes. Products that need $50–300M in scale-up capital (the sweet spot for public-private leverage) score highest for action priority.

Axis 3: Speed-to-Impact (How fast can we close this gap?)

Key Inputs:

This axis addresses political and economic reality: decision-makers in both government and the private sector need wins within 3–5 years, not 15.

Existing domestic capability—Products where SMMs already have partial capability (MRL 5–7) but need capital and demand signals to reach full production (MRL 8–10) are fastest to impact. 93% of U.S. manufacturers have fewer than 100 employees — many already possess latent capacity.

Demand certainty—Products with identified federal procurement demand (DoD, DOE, GSA) or strong commercial pull can reach revenue faster. Government incentives were the #1 cited factor driving reshoring in 2024.

Regulatory runway—Products with clear regulatory pathways (vs. those requiring years of FDA or EPA approvals) move faster.

Proven reshoring trajectory—Some sectors are already moving. Transportation equipment reshoring is up 139% year-over-year, plastics and rubber up 126%, medical equipment up 39%. Sectors with momentum deserve accelerated investment.

The weighting is deliberate. Strategic vulnerability carries half the total weight because the entire framework exists to address national security and supply chain resilience. Economic viability carries 30% because a gap that cannot be closed cost-effectively is not a gap — it is a fantasy. Speed-to-impact carries 20% because political and investor patience is finite and wins beget wins.

Applying the Framework: Where the Data Points

When you apply this scoring matrix to the inventory I have laid out in the preceding sections, several categories immediately surface as Tier 1, with high scores across all three axes.

Chemical intermediates: cyanamide, sarcosine, DCD, guanidine derivatives, pharmaceutical precursors, these score near-maximum on strategic vulnerability. Supplier concentration above 75% for a single country. Defense and pharmaceutical dependencies across multiple downstream products. Zero domestic production for most compounds. They score high on economic viability: $50–300 million scale-up range, existing process chemistry knowledge in the United States, strong TCO case when quality risk, supply disruption risk, and purity requirements are priced in. Process innovations and automation — including the work my company is doing — are closing the cost gap with Chinese production for the first time.

And they score high on speed-to-impact: the chemistry is proven, commercial demand exists today in nutraceuticals, pharma, agriculture, and defense, and the regulatory pathway for industrial chemicals is 18–24 months, not five to seven years.

Large-capacity battery materials: graphite processing, manganese sulfate, lithium refining, electrolyte production. China holds 76% market share in large-capacity batteries. Massive IRA and CHIPS Act incentives are already flowing into battery gigafactories. Electrical equipment accounts for 31% of reshoring jobs in the 2024 data. The reshoring of battery cell manufacturing is already in motion — but the upstream materials processing that feeds those gigafactories remains almost entirely foreign. You can build every battery cell plant the IRA incentivizes and still depend on China for the processed materials that go inside them.

Critical mineral processing scores maximum on strategic vulnerability. China dominates processing for 29 critical minerals. But the key insight, and the one that connects this category directly to the Missing Middle thesis, is that the gap is not mining. The U.S. mines rare earths at Mountain Pass. It mines lithium in Nevada. It has antimony in Montana and Idaho. The gap is processing. The conversion of raw ore into refined, usable material.

That is an intermediate processing step. It is Layer 2 and Layer 3 of the pyramid.

Active pharmaceutical ingredients score maximum on vulnerability. over 50% import share, high concentration from Asia and Europe, national health security imperative that the COVID pandemic made viscerally clear to every American who could not find basic medications on pharmacy shelves.

Economic viability is strong, API manufacturing is well-understood chemistry with established process economics.

But speed-to-impact is slower due to FDA regulatory timelines, cGMP facility validation requirements, and the multi-year qualification cycles that pharmaceutical companies require before switching API suppliers.

This category is Tier 1 on urgency but demands a longer planning horizon.

Mature-node semiconductors round out Tier 1.

Only 6–9% of mature logic chips, the workhorses of automotive, industrial, medical, and defense electronics, are made domestically. CHIPS Act funding is active and facilities are under construction.

But workforce constraints, the 3–5 year facility build timelines, and the enormous capital requirements ($10–20 billion per fab) push this toward the longer and more capital-intensive end of the speed and viability axes. The CHIPS Act addressed this category directly. What it did not address is the upstream chemical supply chain those fabs depend on, the electronic-grade chemicals, ALD precursors, fluorinated gases, and laminate hardeners sourced from Asia.

The Practical Starting Playbook

Identifying the gap is step one. Closing it requires a sequenced playbook that works for government program officers, private equity investors, and founder-operators simultaneously. Here are the six steps, in order.

Step 1: Map the supply chain at the input level, not the industry level.

This is the Fed’s most actionable insight. Industry-level trade data masks input-level risk. The automobile industry looks diversified in aggregate until you examine semiconductor and electronic component sourcing specifically, and discover that a single fab shutdown in Taiwan can idle every auto plant in North America.

Every Tier 1 category in this framework needs an input-by-input vulnerability map that goes at least three tiers deep into the supply chain. If you stop at the first tier, you will miss the chokepoints that actually kill you.

Step 2: Run Total Cost of Ownership analysis against each priority input.

The Reshoring Initiative’s TCO Estimator is free and publicly available. It quantifies the true cost gap including the 30+ factors most procurement departments ignore: freight variability, inventory carrying costs imposed by 90-day ocean transit, quality rejection rates, intellectual property leakage, travel and oversight costs, opportunity costs from long lead times, and the catastrophic tail risk of supply disruption.

Start with inputs that already have chronic delivery problems, quality complaints, or IP concerns, that is where TCO most strongly favors domestic production, and where you will find the easiest business cases to build.

Step 3: Identify existing small and medium manufacturers at MRL 5–7.

This is where NIST’s Manufacturing Extension Partnership (MEP) Supplier Scouting capability becomes critical.

The MEP network operates in all 50 states and has the ability to match federal agency and OEM needs to existing domestic manufacturing capacity. The gap is not always that no one in America can make the product. It is that no one can make it at the volume, purity, or consistency required, and that the capital to bridge that gap has never been available.

Finding the SMM that is already at MRL 6 and giving it the capital, demand signal, and technical assistance to reach MRL 9 is faster, cheaper, and lower-risk than building from zero.

Step 4: Stack the capital.

No single funding source is sufficient to finance a first-of-kind intermediate manufacturing facility.

The architecture requires a blended capital stack that combines multiple sources: OSC loans at $10–150 million for defense-relevant manufacturing, EXIM Bank Make More in America financing for export-competitive production, Section 45X Advanced Manufacturing Production Tax Credits for qualifying materials, DOE Loan Programs Office financing for energy-related manufacturing, USDA loan guarantees for agricultural chemical production, state-level incentives (tax abatements, infrastructure grants, workforce training subsidies), and private capital (venture, growth equity, project finance, strategic investment from downstream customers).

The goal is to bring the blended cost of scaling capital below 5%, making domestic production investment competitive with the subsidized capital available to Chinese state-backed competitors. This capital stacking is not theoretical. These programs are live, funded, and accepting applications. The challenge is navigating the application processes simultaneously and structuring them into a coherent financing package. This is an opportunity unto itself in streamlining capital access.

Step 5: Anchor demand. No manufacturer, not a startup, not a mid-size firm, not a multinational, will blindly invest $50–300 million in a first-of-kind domestic facility on speculative demand. The demand signal must come first or simultaneously with the capital.

This means advance purchase commitments or multi-year procurement contracts from the Department of Defense, the Department of Energy, the General Services Administration, or large commercial OEMs who need supply chain security. The mechanism already exists: DoD’s Other Transaction Agreements (OTAs), Title III of the Defense Production Act, and commercial supply agreements with domestic content requirements. The Reshoring Initiative’s data confirms this: government incentives, including procurement commitments, were the number one factor cited by companies making reshoring decisions in 2024. When the demand signal is clear, the capital follows.

Step 6: Build the workforce in parallel, not in sequence.

The single biggest operational mistake in reshoring is waiting until the factory is built to start training workers. By the time a $100 million facility is constructed, commissioned, and ready for production, typically 24–36 months, it needs trained operators on day one.

Community college manufacturing training academies, registered apprenticeship programs, and employer-sponsored technical training should launch 18–24 months before production begins. This means workforce development starts at the same time as construction, not after it. States that understand this, and that have community college systems willing to build custom training programs in partnership with manufacturers, have a structural advantage in competing for facility siting.

Why This Framework Works for Both Audiences

The scoring matrix is deliberately designed to be legible to both government and private sector decision-makers simultaneously.

Government officials see national security, supply chain resilience, defense industrial base dependency, and job creation metrics weighted into the model, providing the analytical justification for public capital deployment, procurement commitments, and regulatory prioritization.

Private sector operators see TCO analysis, MRL staging, demand certainty, capital efficiency, and workforce availability, the inputs that drive investment committee decisions and facility siting calculations.

Neither side has to take the other’s word for it. The framework uses publicly available data, Federal Reserve SRI methodology, USGS Mineral Commodity Summaries, Reshoring Initiative statistics, BEA input-output tables, DoD MRL assessments— that both sides can independently verify.

This matters because the Missing Middle will not be closed by government alone or by the private sector alone. It requires coordinated action: public capital de-risking private investment, procurement commitments underwriting demand, workforce programs matching facility timelines, and founders willing to build the companies that operate at the intersection of all three.

The framework exists to make that coordination possible.

The question is not whether the tools exist to close the Missing Middle. It is whether anyone assembles them into a coherent strategy and executes.

The Case for Founders

If you are a builder, an engineer, a chemist, an entrepreneur, the Missing Middle is the most underleveraged opportunity in the American economy.

The founders who rebuild the Missing Middle will not look like typical startup founders. They will be chemists, process engineers, and industrialists. They will raise more capital, on longer timescales. The businesses they build will likely not have the growth curves of SaaS companies. They will have something better: structural moats, government incentives, long-term supply contracts, and competitive positioning that takes a decade for anyone to replicate.

It is harder than software. But the opportunity is proportional to the difficulty. A domestic manufacturer with process IP, automation, and regulatory approvals becomes a node in the national supply chain that all levels of buyers depend on.

What Comes Next

The Missing Middle will not rebuild itself by accident. Markets do not spontaneously regenerate industrial capability that was lost over decades.

But the calculus is changing. Process innovation and automation is closing the cost gap. Policy is creating incentives. Geopolitical risk is repricing the cost of foreign dependence. China is not standing still, the CCP knows their leverage.

But, a generation of American builders is starting to look at physical industry with the same ambition the previous generation brought to software.

The window is open. It will not stay open indefinitely. The companies that establish production in the next 3–5 years will have first-mover advantages that compound for decades.

I started a nitrogen chemicals company because I followed a supply chain backward and found a void where American manufacturing used to be. The pattern is everywhere. It is in pharmaceutical intermediates and antibiotic fermentation. It is in semiconductor precursors and PCB laminates. It is in rare earth processing, battery materials, titanium sponge, and munitions chemistry.

This moment in time is America’s Ad Astra opportunity to seize destiny. We have the raw materials, we have the intellectual talent and inventions. Its time to integrate.

Its time to BUILD.

Thank you for reading.

Fantastic article, genuinely learned a lot. Would love to read more content like this.